|

|

|

|

Relief for taxpayers in income tax search and requisition cases as government amends the Finance Bill 2025

Mar 25, 2025

Synopsis

Income Tax: The govt said: "The word ‘total income’ has been replaced with ‘total undisclosed income’ in the marginal heading and in sub-section (1) and sub-section (7) of section 158BA.... The concept of assessment of total income has been replaced with the assessment of undisclosed income. This reflects a paradigm shift where the main objective of a search or requisition is to identify income that has not been disclosed."

With an aim to give relief to income taxpayers, the government has amended the provisions dealing with income tax search cases, as per a supplementary frequently asked question (FAQ) released by the Income Tax Department. In the amended Section 158BA (Assessment of undisclosed income as a result of search), the word ‘total income’ has been replaced with ‘total undisclosed income’.

Read below to know more about how taxpayers get relief due to this amendment in Finance Bill, 2025

How did taxpayers get relief in case of income tax search or requisition cases through amendment in Chapter XIV-B?

Chapter XIV-B which relates to the special procedure to be followed for Income tax search cases, has also been amended and now it implies that the main objective of the government is to conduct an income tax search or requisition operation to identify income that has not been disclosed and not regular disclosed income.

The Income Tax Department said: “The concept of assessment of total income has been replaced with the assessment of undisclosed income. This reflects a paradigm shift where the main objective of a search or requisition is to identify income that has not been disclosed.”

The government now trusts that you will disclose regular income in the block income tax return. At present, you are required to file a block ITR in pursuance of a notice under Section 158BC within the time specified in the tax notice, which shall not exceed 60 days.

“...The changes to Chapter XIV-B aim to focus only on assessing undisclosed income and place trust in the taxpayer to disclose regular income in the block income tax return,” said the Income Tax Department.

Experts say now with this amendment the government has helped in giving clarity to taxpayers and removes ambiguities which previously caused unnecessary harassment of taxpayers.

CA Ashish Niraj, Partner, A S N & Company, says “This amendment is a welcome step from the perspective of Taxpayers. In the budget 2025 itself the finance minister had talked about “trust first, scrutinise later” and on that same line by replacing word “total” with “undisclosed” in chapter XIV-B ,the government is showing faith in taxpayers that they must have reported regular income in their ITR. Now the scope of the chapter has been narrowed to focus only on undisclosed income parts.”

Mihir Tanna, associate director, S.K Patodia & Associates LLP says: "As per the old provisions, the term "total income" is used, which creates the impression that normal income might also be required to be disclosed in the return to be filed post search.To maintain consistency, it provides that only undisclosed income declared in the return shall be included in the total income of the block period. Accordingly, total income declared in a original return is not subject to the 60% tax rate applicable on undisclosed income."

Income tax department to compare your last year ITR with current year’s ITR for any irregularities: How taxpayers will be impacted?

Read below to know the other amendments details

FAQs about other amendments to Income tax search cases

As per a supplementary FAQ to the Finance Bill, 2025 here are the details:

Amendments Related to Chapter XIV-B of the Income-tax Act, 1961

Q.1 What amendment has been made in respect of chapter XIV-B of Income-tax Act, 1961?

Answer: The concept of assessment of total income has been replaced with the assessment of undisclosed income. This reflects a paradigm shift where the main objective of a search or requisition is to identify income that has not been disclosed.

However, the pending proceeding of any year comprised in the block period is abated and is assessed along with the block assessment. Hence, the AO shall be at liberty to compute undisclosed income on the basis of evidence found as a result of search or requisition as well as any other material or information as is available with him or come to his notice.

Regular income will continue to be determined based on entries or transactions recorded in the books of account or documents maintained in the normal course before the initiation of the search or requisition. The changes to Chapter XIV-B aim to focus only on assessing undisclosed income and place trust in the taxpayer to disclose regular income in the block income tax return.

Q.2 What amendment has been made in respect of section 158BA of Income-tax Act, 1961?

Answer: The word ‘total income’ has been replaced with ‘total undisclosed income’ in the marginal heading and in sub-section (1) and sub-section (7) of section 158BA.

Q.3 What income shall not form part of undisclosed income as per section 158BB of Income-tax Act, 1961?

Answer: The following income shall not be included in the total undisclosed income of the block period:

a) Total income determined under section 143(1), or assessed under sections 143(3), 144, 147, 153A, 153C, or assessed earlier under section 158BC(1)(c) or section 245D(4), prior to the date of initiation of the search or requisition;

b) Total income declared in the return filed under section 139 or in response to a notice under section 142(1), prior to the date of the search or requisition, and not covered under clause (a);

c) Income computed by the assessee for the specified period based on books of account maintained in the normal course;

d) Total income referred to in section 115A(5), section 115G, or section 194P(1).

Q4. What amendment has been made in respect of undisclosed income as per section 158BB of the Income-tax Act, 1961?

Answer: . The total undisclosed income referred to in section 158BA(1) for the block period shall be the aggregate of the following:

a) Undisclosed income declared in the return furnished under section 158BC;

b) Undisclosed income determined by the Assessing Officer under sub-section (2)

Q.5 What are the primary conditions to be fulfilled for requesting for extension of time allowed for furnishing block return?

Answer:. The time allowed for furnishing a return under section 158BC(1)(a) can be extended by 30 days if all the following conditions are met:

1.The previous year immediately precedes the year in which the search or requisition was made, and the due date for furnishing return for that year had not expired before the search or requisition;

2.The assessee was liable for audit under section 44AB for that previous year;

3.The accounts of that year (maintained in the normal course) were not audited on the date of issuance of the notice; and

4.The assessee makes a written request for extension of time for furnishing the block return to get such accounts audited.

Q6. What amendment has been made in respect of section 158BB of Income-tax Act, 1961?

Answer: Section 158BB has been amended to provide a clear distinction between disclosed and undisclosed income and to compute the assessment of total undisclosed income.

Q.7 How will the tax referred to in section 158BA(7) of Income-tax Act, 1961 be charged as per section 158BB of Income-tax Act, 1961?

Answer: The tax referred to in section 158BA(7) shall be charged on the total undisclosed income determined in the manner specified in section 158BB(1).

Q.8 Is there any provision for getting books of account audited in respect of a previous year immediately preceding the previous year in which the search is initiated or requisition is made and the due date for furnishing the return has not expired prior to the date of initiation of the search or the date of requisition?

Answer: Yes. Under the fifth proviso to section 158BC(1)(a), a taxpayer can request an additional 30 days to get the books of account audited for the previous year immediately preceding the year in which the search or requisition is initiated, provided the due date for filing the return for that year had not yet expired on the date of the search or requisition.

Q.9 What amendments have been made in respect of section 158BD of Income-tax Act, 1961?

Answer: The block period has been clearly defined in respect of another person covered under section 158BD. There are two cases:

Where there is one specified person relevant to such other person, the block period for such other person shall be the same as that for the specified person;

Where there is more than one specified person relevant to such other person, the block period shall be the same as that of the specified person whose block period ends on the later date.

Q.11 What amendments have been brought in respect of abatement in section 158BD of Income-tax Act, 1961?

Answer: In the case of a person covered under section 158BD, for the purpose of abatement under section 158BA(2) and 158BA(3), the reference to the date of initiation of search or requisition shall mean the date on which money, bullion, jewellery, virtual digital assets, or other valuable items, or books of account, documents, or other materials relating to undisclosed income were received by the Assessing Officer having jurisdiction over such person.

Q.12 What amendment has been made in respect of the time-limit for completing assessment under section 158BE of Income-tax Act, 1961?

Answer. The time-limit for completion of block assessment is twelve months from the end of the quarter in which the last of the authorizations for search or requisition has been executed. However, if the time allowed under section 158BC(1)(a) is extended by an additional 30 days under the fifth proviso, the time-limit for completion of the block assessment shall be thirteen months from the end of the quarter in which the last of the authorizations was executed.

Q.13 What amendments have been made in respect of section 113 of Income-tax Act, 1961?

Answer: The word ‘total income’ has been replaced with ‘total undisclosed income’ so that the total undisclosed income of the block period, determined under section 158BC, shall be chargeable to tax at the rate of sixty per cent.

Amendment to Section 158BB(1A)

According to Taxmann research published document, "A new clause (d) has been introduced in Section 158BB(1A) [inserted by Finance Bill (Lok Sabha)] that the income of certain assesses shall be considered disclosed income where return filing for them is not mandatory and the tax is deducted from such income. The incomes that shall be considered disclosed income under this provision shall be as follows:

Where the total income of a non-resident or a foreign company consists only of incomes specified under Section 115A (i.e., interest, dividend, royalty, FTS.)

Where the total income of an NRI consists only of income derived from foreign exchange assets1 or longterm capital gain arising from the transfer of such assets and is taxable under the special regime provided in Chapter XIIA (Section 115C to 115-I).

Where the total income of a resident senior citizen consists of the pension income and interest income received or receivable from any account maintained in the bank responsible for deduction of tax under Section 194P.

New mechanism to compute the undisclosed income under Section 158BB

According to Taxmann research published document, The Finance Bill (Lok Sabha) provides a new methodology to compute the undisclosed income for the block assessment with retrospective effect from September 1, 2024 by inserting sub-section (1A), substituting sub-sections (1), (3) and (5), amending sub-section (2) and omitting sub-section (6). The new provision does not follow the circuitous method of first computing the total income, including disclosed and undisclosed income, and then reducing the disclosed income from such total income. It provides a straightforward method to compute the undisclosed income, which shall be the aggregate of undisclosed income declared by the assessee and determined by the assessing officer. The new methodology for the computation of undisclosed income under Section 158BB has been discussed below.

Section 158BB contains the following provisions for the computation of total undisclosed income of the block period:

Finance Bill (Lok Sabha) substituted the provisions of Section 158BB(1) to provide that the undisclosed income shall be the aggregate of undisclosed income declared by the assessee and determined by the assessing officer.

A sub-section (1A) has been inserted to exclude the disclosed income while computing the total undisclosed income. This sub-section contains clauses (a) to (d) defining which income shall be considered as disclosed income and to be excluded while computing the undisclosed income for the purpose of this Chapter. Previously, such exclusion was made under Section 158BB(5).

Section 158BB(2) provides that the undisclosed income falling within the block period shall be computed based on evidence found. Finance Bill (Lok Sabha) has made a consequential amendment to this provision due to the new method prescribed in sub-section (1) to compute undisclosed income.

Section 158BB(3) provides that the evidence relating to international transactions or specified domestic transactions for the specified period shall be ignored when determining the total income. There is no change in this provision by the Finance Bill (Lok Sabha).

Section 158BB(4) contains a special provision for determining the undisclosed income in the case of a partnership firm. It also provides that the provisions of Sections 68 to 69C and Section 92CA shall apply as relevant to the block period. There is no amendment to this provision by the Finance Bill 2025 or Finance Bill (Lok Sabha).

Section 158BB(5) specifies that the undisclosed income computed after reducing the disclosed income from total income will be charged to the tax at the rate specified under Section 113. Finance Bill (Lok Sabha) has made a consequential amendment to this provision due to the new method prescribed in subsection (1) to compute undisclosed income.

Section 158BB(6) specifies that where the income declared as per Section 158BB(1) is a loss, it shall be ignored. The Finance Bill (Lok Sabha) has omitted this provision. This omission will not impact the prohibition against set-off of losses against the undisclosed income as provided in Section 158BB(7).

Section 158BB(7) prohibits the set-off of carried forward losses and unabsorbed depreciation against the undisclosed income. There is no amendment to this provision by the Finance Bill 2025 or Finance Bill (Lok Sabha)

[The Economic Times]

Taxmen to assess only undisclosed income in search cases: Finance Bill

New Delhi, Mar 25, 2025

The amendment, which was approved by the Lok Sabha on Tuesday, will be made effective retrospectively from September 1, 2024

The government has proposed amendments to Finance Bill, 2025, under which tax officers will determine only undisclosed income for block assessments in search cases and not total income of the assessee.

The amendment, which was approved by the Lok Sabha on Tuesday, will be made effective retrospectively from September 1, 2024.

The government has brought in amendments to Chapter XIV-B of Income Tax Act through which the concept of assessment of 'total income' has been replaced with the assessment of 'undisclosed income'.

This amendment was part of the 35 amendments that the Lok Sabha approved to the Finance Bill, 2025, on Tuesday. This reflects a paradigm shift where the main objective of a search or requisition is to identify income that has not been disclosed, an FAQ issued by the income tax department said.

"The changes to Chapter XIV-B aim to focus only on assessing undisclosed income and place trust in the taxpayer to disclose regular income in the block income tax return," the FAQ said.

According to the FAQ, the regular income of the assessee facing an assessment following a search operation will be taxed separately at the applicable rate.

Regular income will continue to be determined based on entries or transactions recorded in the books of account or documents maintained in the normal course before the initiation of the search or requisition, the FAQ said.

EY in its analysis of Finance Bill, 2025, amendments said that last year, the government introduced a significant shift in search assessments from assessment of each individual year separately to a single consolidated assessment for a block period comprising specified years.

In this regard, the New Block Assessment Regime provided for assessment of undisclosed income, as well as regular income.

According to EY, the amended Finance Bill, 2025, in a way, now reinstates the pre-2003 block assessment regime to restrict the scope of assessment under the New Block Assessment Regime to only undisclosed income.

[Press Trust of India]

Lok Sabha passes Finance Bill 2025 with 35 amendments, Rajya Sabha next

Mar 25, 2025

The amendments include one that abolishes a 6 per cent digital tax, popularly known as the 'Google Tax,' on online advertisements

The Lok Sabha on Tuesday passed the Finance Bill, 2025 with 35 amendments. The amendments include one that abolishes a 6 per cent digital tax, popularly known as the 'Google Tax,' on online advertisements.

"I have proposed to remove the 6 per cent equalisation levy for advertisements. Equalisation levy on online advertisements to be abolished to address uncertainty in international economic condition," said Sitharaman while replying to the discussions on the Finance Bill 2025 in the Lok Sabha,.

Earlier today, Sitharaman presented the amended Finance Bill 2025 in Parliament, seeking approval for key Budget proposals.

"Finance Bill, 2025, provides unprecedented tax relief to honour taxpayers," the finance minister said.

On February 1, Sitharaman presented the Union Budget with a total expenditure of Rs 50.65 trillion, an increase of 7.4 per cent over the revised estimate of Rs 47.16 lakh crore for the current fiscal year 2024-25.

Rs 5,41,850.21 crore has been allocated for Centrally Sponsored Schemes (CSS) for FY26 compared to Rs 4,15,356.25 crore for FY25.

The fiscal deficit for FY26 is projected at 4.4 per cent against 4.8 per cent in the current FY25.

With the passage of the Finance Bill 2025, the Lok Sabha has concluded its role in the Budget approval process. The Bill will now move to the Rajya Sabha for consideration. After the Rajya Sabha approves the Bill, the Budget process for 2025-26 will be complete.

New Income Tax Bill to be discussed in Monsoon Session

FM told Parliament that the new Income Tax Bill will be taken up for discussion in the Monsoon Session, which will start in July. She said the Bill, which was introduced in the House on February 13, is currently being vetted by the Select Committee.

"The new Income Tax Bill brought during this Budget session, we hope will be taken up for discussion in this House during the Monsoon session, " said Sitharaman in Lok Sabha today.

[The Business Standard]

Budget changes: Will capitals gains make you ineligible for tax rebate?

New Delhi, Feb 21, 2025

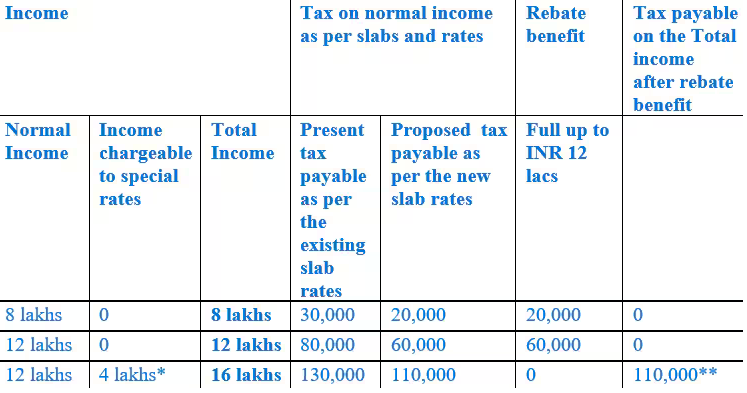

Pre-Budget 2025, taxpayers could claim the rebate if their total income was Rs 7 lakh or below. However, with the new Budget, this limit has been increased to Rs 12 lakh

For many taxpayers, the Section 87A rebate under the Income Tax Act has been a valuable relief, reducing the overall tax liability, especially for those with an income of Rs 7 lakh or less. However, the Union Budget 2025 has introduced significant changes that could affect how you claim this rebate.

What’s Changed in Budget 2025?

The most notable change is the increase in the income threshold for claiming the rebate. Pre-Budget 2025, taxpayers could claim the rebate if their total income was Rs 7 lakh or below. However, with the new Budget, this limit has been increased to Rs 12 lakh, which is great news for many taxpayers. This means more people will be eligible to receive the tax rebate of up to Rs 60,000.

But, there’s a catch: The rebate will no longer apply to special income—such as capital gains—that is subject to tax at special rates. In simpler terms, if your total income includes capital gains, the rebate won’t apply to that portion of your income.

How Does This Work in Practice?

Ritika Nayyar, Partner, Singhania & Co, simplifies this for you:

Example 1: Total Income Rs 12 lakh, No Special Income

Imagine you have a total income of Rs 12 lakh for the year. This could be a combination of your salary and other normal income sources. Under the old system, you would have been eligible for a Rs 25,000 rebate if your income was below Rs 7 lakh, but now, with the new budget, you can claim a rebate of up to Rs 60,000 because the limit has increased to Rs 12 lakh. This means you pay less tax, which is a positive change.

Example 2: Total Income Rs 12 Lakh with Rs 2 Lakh in Capital Gains

Now, let’s assume your total income is Rs 12 lakh, but Rs 2 lakh of that comes from long-term capital gains, which are subject to special tax rates. In this case, the capital gains portion won’t be eligible for the rebate, as it's taxed at special rates.

So, if your normal income is Rs 10 lakh (after excluding the Rs 2 lakh capital gains), you can claim a rebate on that amount, reducing your tax liability for the normal income. However, the Rs 2 lakh in capital gains will be taxed separately, and the rebate won’t apply to this amount. Therefore, the overall tax you owe will still be lower, but you’ll have to pay tax on the capital gains separately, which is a key change.

Example 3: Total Income Rs 13 Lakh with Rs 3 Lakh in Capital Gains

What if your total income crosses the Rs 12 lakh threshold, and you also have some capital gains? For instance, with a total income of Rs 13 lakh, of which Rs 3 lakh is from capital gains, you would not be entitled to any rebate. Even though your normal income could have been eligible for a rebate under the old system, the total income now exceeds the threshold of Rs 12 lakh, disqualifying you from the rebate.

"In essence if the intent of law was to actually provide relief, despite of excluding the special income, there ought to be relaxation that for claiming the rebate the normal total income excluding capital gains should be below Rs 12 lakh limit. Since the above approach does not seem prudent for taxpayers or be the intent of law to just snatch away the whole benefit just because you have an element of special income in it," said Singhania.

SR Patnaik, Partner (head - taxation), Cyril Amarchand Mangaldas, breaks this down further:

*Assuming long term capital gains tax payable @12.5% amounting to Rs 50,000.

** Exclusive of applicable surcharge and education cess

"Hence, assuming that the proposed changes to the IT Act are passed as is, the rebate provisions shall be available only in respect of the income tax computed on the normal income. However, if the total income of the taxpayer exceeds the minimum threshold limit, then the taxpayer shall be liable to pay on the total income without being entitled to the rebate available under section 87A, as being demonstrated in the above table," said Patnaik.

This shows how important it is to consider both the total income and the components of your income when planning your taxes. If your capital gains push your income over the threshold, you’ll lose the benefit of the Section 87A rebate.

Should You Be Concerned?

If you’re someone who relies on the Section 87A rebate to reduce your tax burden, these changes could impact you, especially if your income includes significant capital gains. While the increase in the income limit to Rs 12 lakh is a welcome change, the exclusion of special income from the rebate may feel like a disadvantage, particularly if your total income barely crosses the threshold due to capital gains.

In essence, the budget’s intent is to simplify and clarify the rules, but it does make it slightly more complicated for those with mixed income sources. To fully benefit from the rebate, you’ll need to ensure that your normal income (excluding capital gains) remains under Rs 12 lakh.

What Can You Do?

Taxpayers with mixed income, especially capital gains, should start reviewing their income sources more carefully. If your income is close to the threshold, consider tax planning strategies to minimize capital gains or adjust other aspects of your income to ensure eligibility for the rebate.

"For taxpayers having total income below Rs 5 Lakhs in the old regime or Rs 7 Lakhs in the new regime, rebate u/s 87A is available to the extent of 100% of the tax payable (for FY 2025-26 onwards, the said limit is Rs 12 Lakhs under the new regime). While the said section does not provide for any exceptions to the kind of income that may be considered for computing the rebate, Section 112A, which provides for the tax liability on long term capital gains arising out of sale of listed equity shares as well as equity-oriented schemes of mutual funds, states that rebate u/s 87A shall not be available on the tax liability arising thereon.

Accordingly, it can be concluded that rebate shall be applicable all kinds of income including long term capital gains on sale of capital assets other than listed equity shares or equity-oriented mutual funds," said Rajarshi Dasgupta, Executive Director-Tax, AQUILAW.

[The Business Standard]

Budget 2025:

MSME definition revision a ‘good decision,’ says India Inc; seeks more ‘aha moments’ for ease of doing business

Feb 10, 2025

Synopsis

Experts have hailed certain measures announced in the Budget aimed at supporting MSMEs and exports; however, they are advocating for further streamlining of processes that can enable ease in customs and regulatory updates.

The Union Budget 2025-26, announced by Finance Minister Nirmala Sitharaman on February 1, 2025, introduced a host of measures aimed at supporting India Inc., with an emphasis on tax reforms, export promotion, and ease of doing business being paramount. A revision in MSME classification, steps to boost India’s share in global trade, and improving the regulatory landscape got notable mentions, among other key highlights.

Announcing a series of measures to strengthen the MSME sector—often referred to as the backbone of the economy—the Budget acknowledged the sector’s vital role as one of the key engines for India’s growth, along with agriculture, investments, and exports.

“To help MSMEs scale operations and access better resources, the investment and turnover limits foBudget 2025: MSME definition revision a ‘good decision,’ says India Inc; seeks more ‘aha moments’ for ease of doing businessr classification have been increased by 2.5 times and 2 times, respectively. This is expected to improve efficiency, technological adoption, and employment generation,” a post-Budget PIB release stated.

Rationalisation of MSME Definition

Speaking to ET Digital in an in-depth analysis of the budgetary announcements, Anil Bhardwaj, Secretary General, Federation of Indian Micro and Small & Medium Enterprises (FISME), discusses how these measures will benefit the sector. “From 2020 to 2024, the raw material prices have increased tremendously. Take the example of gold, which has seen a rise of over 30%. Similarly, this has been the case for steel and copper. So, all these small enterprises became medium enterprises, and they were elbowed out from the public procurement since the 25% set aside is available only for micro and small enterprises. Similarly, for gem & jewellery exporters, they were suddenly unable to access funds allocated to MSMEs due to gold prices. So, a rationalisation of the definition was necessary,” he explains.

According to him, tying a definition to turnover directly links it to raw material costs. “For instance, there are thousands of units that produce AC conductor wires, where 85-90% is just the raw material cost. If the raw material cost increases by 30%, their turnover will similarly increase by the same percentage, without making any material change to their work. That is why this move was necessary,” he states.

In addition, it will also help them tap funds, especially equity. “Over the past one and a half years, a large number of MSMEs have entered the SME IPO market, securing equity funding and making investments in plants and machinery. The moment they do it, they again move out from micro to small or small to medium and large. This additional doubling of investment and turnover criteria would enable them to make investments, attract funding, and go for value addition. I believe it is a very good decision,” Bhardwaj highlights.

Ease of Doing Business

The Budget also introduced a measure aimed at promoting the ease of doing business by fixing a time limit of two years, which can be extended by a year, for finalising the provisional assessment. “Presently, the Customs Act, 1962, does not provide any time limit to finalise provisional assessments leading to uncertainty and cost to trade. I propose to introduce a new provision that will enable importers or exporters, after clearance of goods, to voluntarily declare material facts and pay duty with interest but without penalty. This will incentivise voluntary compliance,” said FM Sitharaman as part of her Budget speech.

This is one of the series of steps as far as trade facilitation is concerned and should not be treated in isolation, says M.S. Mani, Partner, Deloitte India. “To increase exports, we have to do a lot of liberalisation in respect of the export procedures. We have to bear in mind that the goods that we are exporting, the products that we are exporting, many of them have significant import content. Many of them are not 100% organically manufactured in India. So, the import of the components and the import of the sub-assemblies are intricately linked to the export of the finished product. Therefore, when we do import liberalisation, it also has a significant impact in terms of our ability to export, not only from a logistics point of view but also from a cost point of view,” he says, adding that provisional assessment being done in two years should also serve as an example for other procedures in Customs which should also have a specified time limit.

Extending the emphasis on ease of doing business, the Budget 2025 had announced a ‘High-Level Committee for Regulatory Reforms’ to be set up for a review of all non-financial sector regulations, certifications, licenses, and permissions. “The committee will be expected to make recommendations within a year. The objective is to strengthen trust-based economic governance and take transformational measures to enhance ‘ease of doing business,’ especially in matters of inspections and compliances. States will be encouraged to join in this endeavour,” the Budget document stated.

Rishi Agrawal, CEO of TeamLease Regtech, adopts a cautionary tone regarding the announcement. He acknowledges that while it is a “welcome step,” there is always a risk that such reports get delayed and never translate into actionable reforms.

“It will be interesting to see what the committee comes out with, but one of the areas where the government has already done a lot of work is labour reform. Labour is the elephant in the room. Over 50% of the compliance for an MSME comes from labour; the current labour laws are archaic. The 21st-century Indian entrepreneur needs a new framework for legal laws. So, a lot of legislative and executive actions have been taken. I would like the committee to expedite how we can take the body of work that has been put together in the past few years to fruition. So, that is certainly an area where I would like to see some action,” he says.

Enhancing Exports

Another focus area in the Budget announcements was a series of steps to enhance exports; highlights included a digital public infrastructure, ‘BharatTradeNet,’ proposed as a unified platform for international trade documentation and financing solutions. According to GTRI Founder Ajay Srivastava, such a platform can be a super game changer for the ecosystem. “Today all our regulatory interfaces are department-centric. An exporter has to approach at least 10-15 departments. If we make it user- or exporter-centric, there will only be one interface through which the exporter has to operate. This simplification will allow the shift of many MSMEs, who are doing business domestically, to become exporters. It can do wonders for the Indian economy,” he states.

Hits and misses

Experts believe that the Budget 2025 includes measures that tackle numerous crucial aspects, yet certain expectations remain unfulfilled. “In respect of Customs, for quite some time, we have been hearing that there is a benchmarking exercise, which the government has done in the past in respect of comparing India’s trade facilitation measures with other countries. If we compare ourselves with some of the good countries in Europe, it may be a good measure to benchmark ourselves with them and have a time frame of five years or 10 years. That is one expectation that I would have from this Budget or the subsequent Budgets,” Mani says.

Others root for the formation of a group to examine the simplification process of a sectoral nature. “For example, steel and textiles. Steel imports account for just 6% of our consumption. But look at how we are regulating imports. So, such problems exist not only in steel, textile or chemical sectors. I am very sure that if we can handle the task for three or four ministries, our GDP rate will increase by at least 2% very soon,” Srivastava adds.

Industry experts also say that the Budget is a good opportunity to reaffirm the commitment before the internal and external audience. Bhardwaj says that having clarity as a nation will be of utmost importance. “Do we want protection or openness? The message has to be clear – you can’t really ride these two forces together. I think there is a need to reaffirm that we want openness, privatization. We want Indian entrepreneurship to unleash itself to make India a rich country. Unless there is full conviction on these fundamental issues, we will have confusion,” he states.

On a closing note, Agrawal emphasises aspects that can streamline processes further as far as regulatory updates are concerned. “There are over 2,000 websites that publish regulatory updates. Finding regulatory updates for an entrepreneur, especially a multi-state entrepreneur, is a nightmare. There are over 9,000 regulatory changes that affect doing business in the country, and there is no single source of proof. This has created a lot of information asymmetry. I would have loved to see some budgetary allocation to creating a searchable, sortable and filterable common portal for regulatory updates,” he states.

Lastly, he talks about creating an ‘aha’ moment for ease of doing business to reap enriching rewards as an economy. “UPI created an ‘aha’ moment for the country in digital payments. We need to do a similar ‘aha’ for ease of doing business too; API-enabled filings is one of them. We have already seen the template being created in income tax and GST. We need to extend that to other areas of the government as well. Some budgetary allocation on it would have been great and meant that things are moving forward in that space,” Agrawal adds.

[The Economic Times]

GST rules for credit notes tightened to stop leakage

Mumbai, Feb 3, 2025

A new Budget amendment necessitates suppliers to ensure buyers reverse input tax credits (ITC) before claiming adjustments when issuing a credit note. This change aims to prevent revenue leakage and double tax benefits. The amendment could face legal challenges as it imposes an additional burden on suppliers for the recipient's non-compliance.

A supplier of goods or services can issue a credit note to the buyer in several instances. Typically this happens if the supplier has made mistakes in the original invoice, such as declaring a value higher than the value of goods or services actually provided or has mentioned an incorrect higher GST rate. A credit note is also issued when goods are returned by the buyer.

Rohit Jain, deputy managing partner, at Economic Laws Practice explains, "There exists a possibility that the recipient (buyer) could have taken input tax credit (ITC) based on the original invoice and subsequently, the supplier issues a credit note and claims adjustment (refund). The Budget proposes that it is now necessary for the supplier to ensure that the recipient reverses ITC before such adjustment is claimed."

The amendment appears to have been introduced to prevent revenue leakage. It will prevent scenarios where the supplier claims a reduction in its GST liability, owing to the credit note, but the buyer continues to avail of the corresponding ITC. This results in a double tax benefit with an adverse impact on GST collection.

Jain points out that proposed amendment is based on recommendations of the GST Council. As it places an additional burden on suppliers, there exists a possibility that the amendment may be challenged in courts on the premise that suppliers will have to bear consequences of the recipient's non-compliance, despite having no control over the recipient's actions.

[The Times of India]

Obsolete GST norms on gift coupons deleted

Mumbai, Feb 3, 2025

Following the stipulation in a recent GST council meeting and issue of a circular, Budget 2025 has deleted obsolete provisions relating to goods and services tax (GST) on gift vouchers. However, it should be noted that allied activities like marketing of these vouchers will still be subject to gift tax.

Rohit Jain, deputy managing partner, at Economic Laws Practice said, "The Karnataka high court had held that vouchers do not fall in the category of goods or services and cannot be subject to GST. Subsequently, a circular issued in Dece, stated that GST does not apply on vouchers. Consequently there is no need to determine the time of supply.

The proposed amendment is in line with these developments. However, other services provided by the supplier including redemption of vouchers will be liable to GST and provisions relating to the time of supply will apply."

The time of supply is a norm that determines when GST liability applies for a particular transaction.

[The Times of India]

Budget 2025 focuses on ease of doing biz, promotes manufacturing: ICAI

New Delhi, Feb 1, 2025

The Institute of Chartered Accountants of India (ICAI) on Saturday said the Budget focuses on ease of doing business, promote domestic manufacturing and position India as a more competitive player in global trade, supporting economic resilience and growth.

"Suggestions by ICAI in Pre-Budget memorandum regarding the finance bill 2025, phasing out of alternative tax regime, rationalisation of TDS and TCS regime, exemption of withdrawal from NSS and taxation of business trusts have also been accepted," ICAI President Ranjeet Kumar Agarwal said in a statement.

Finance Minister Nirmala Sitharaman on Saturday presented her eighth consecutive Budget. Sitharaman announced significant income tax cuts for the middle class and unveiled a blueprint for next-generation reforms for Viksit Bharat as she treaded a fine line between fiscal prudence and providing a thrust to growth.

ICAI also said deeming the annual value of two self-occupied house property as nil instead of erstwhile one, is a great move.

Among other measures, the Budget has announced a scheme to make India a global hub for toys by focusing on cluster development.

Contract manufacturing firm Aequs' Chairman and CEO Aravind Melligeri said the continuing tilt towards strengthening India's manufacturing sector is a positive step for growth.

"The all-round emphasis on MSMEs, which the minister termed as the second engine of growth is the backbone of Indian manufacturing, is in the right direction," he said in a statement.

Given the current market conditions and also long-term need to make India a global toy manufacturing hub, Melligeri said the emphasis on clusters for toy manufacturing is welcome.

"Having said that, we are awaiting some PLI announcements in the near future for components for consumer electronics, and manufacturing of toys which will provide a further fillip to Make in India," he added.

The company has a toy manufacturing cluster in Karnataka.

[Press Trust of India]

Crypto income:

Budget 2025 tightens crypto transaction monitoring, other tax norms

Feb 2, 2025

Synopsis

Crypto announcements in Budget 2025: The Budget 2025 has proposed to tighten certain rules for crypto trading. As per the amendments made, income from VDAs will be part of the undisclosed income under the Search and Seizure. Further, the government has inserted new section under the Income Tax Act for mandatory reporting requirements.

Budget 2025 has tightened the norms for taxpayers engaged in cryptocurrency trading. Budget 2025 has put virtual digital assets such as cryptocurrency and NFTs, which will now be part of undisclosed income, attracting higher tax rates. Further, disclosure requirements have been widened for taxpayers having income from crypto trading according to The Times of India report.

In fact, other amendments have been made in this realm, which only tighten the reins for those who engage in crypto trading. For instance, in search cases, virtual digital assets will now be part of undisclosed income, attracting a higher tax rate. Earlier, income from crypto trading was not part of the search and seizure procedure. While taxpayers had to disclose income from crypto trading in income-tax returns, disclosure requirements have widened.

Kunal Vyas, Partner at Gandhi Law Associates, says, "Budget 2025 has inserted new section 285BAA mandating reporting entities dealing in crypto-assets to furnish information on transactions related to such assets. This means that exchanges, intermediaries, or any other prescribed entities will have to report details of crypto transactions to the income-tax authorities. This requirement is similar to the reporting obligations imposed on mutual fund companies, stock exchanges, and other financial institutions for tax compliance purposes."

Aaron Kamath, Leader, Technology and Commercial Law Practice, Nishith Desai Associates says, "The Finance Bill, 2025 presented seeks to clamp down on undisclosed transactions and tighten oversight by broadening the definition of VDAs and obligating reporting entities dealing with crypto-asset transactions to furnish transaction details to the income tax authorities, with the leeway to rectify a defect in reporting within 30 days. The Bill also gives the Government the power to issue rules for entities to register with the income tax authorities, and for them to conduct due diligence to identify crypto users or owners."

The key provisions of Section 285BAA as proposed in Budget 2025 include:

i) Mandatory Reporting: Reporting entities (as prescribed) must submit transaction details in a specified format and within a prescribed timeline.

ii) Correction Mechanism: If the submitted statement is found defective, the concerned entity will be notified and given 30 days (or an extended period) to rectify the issue. If not corrected, it will be treated as inaccurate reporting.

iii) Non-Compliance Consequences: If a required entity fails to submit the statement within the prescribed period, authorities can issue a notice demanding compliance within a specified timeframe.

iv) Self-Disclosure of Errors: If a reporting entity later discovers inaccuracies in the submitted information, it is obligated to inform the tax authorities and provide the correct details.

v) Government Rules & Due Diligence: The Central Government will specify which entities need to register with the tax authorities, what information must be maintained, and what due diligence must be performed to identify crypto users and owners.

Vyas says, "Additionally, the amendment expands the definition of Virtual Digital Assets (VDA) to explicitly include any crypto-asset based on cryptographically secure distributed ledger technology."

Income from crypto trading is currently taxed at 30% and will remain the same for the upcoming financial year. Further, stringent regulation prevents crypto traders from offsetting losses incurred in crypto transactions against profits from other crypto trades or any alternative income sources.

The Organisation for Economic Co-operation and Development has developed a Crypto Assets Reporting Framework, which provides for automatic exchange of tax relevant information on Crypto Assets. India is one of the jurisdictions implementing Automatic Exchange of Information.

[The Economic Times]